Understanding how financial instruments respond to broader market forces is key to building effective macro trading strategies. One concept central to this process is macro beta—a measure of how sensitive a security’s returns are to overarching economic or financial market movements. Traditionally used in equity markets, beta can be extended to macro contexts to help traders reduce unwanted exposure to systemic risk.

In this article, we explore how “beta learning,” a statistical technique, refines macro trading strategies by estimating and mitigating exposure to macroeconomic influences. Using this approach, traders can better isolate the alpha, or strategy-specific return, by adjusting for systematic risks.

Redefining Beta in a Macro Context

Classic beta measures how a single stock reacts to movements in a broader equity index. Macro beta, on the other hand, reflects how a financial contract responds to global economic factors like inflation, market sentiment, or credit risk. These broader influences can often be captured through return data from baskets of derivatives that span equities, credit, or currencies.

The usefulness of macro beta lies in its ability to highlight whether a strategy’s profits are truly driven by unique signals or simply by general market trends. By calculating macro beta, traders can identify and potentially hedge out these market-wide influences.

Why Macro Beta Matters

In many macro strategies, especially those based on individual asset signals, market-wide dynamics can interfere with performance. For instance, an emerging market currency strategy might seem profitable, but much of its return could actually stem from exposure to global equity trends. This not only increases volatility but also undermines diversification and backtest reliability.

To counter this, traders can use macro beta to design hedged strategies—where positions in targeted contracts are paired with offsetting positions in macro factor baskets. This immunization reduces the effect of common market movements, allowing the underlying strategy signals to shine.

Challenges in Estimating Beta

Beta estimation isn’t without pitfalls. If the relationship between a contract and a macro factor is weak or unstable, hedging can introduce new risks, known as basis risk. Additionally, if the contract itself influences the macro factor—like crude oil influencing inflation metrics—reverse causality can render the beta estimate ineffective.

Moreover, poor estimation due to short time series or structural breaks can amplify rather than reduce unwanted exposures. Therefore, robust and adaptive beta estimation methods are essential.

The Role of Statistical Learning

Statistical learning techniques provide a dynamic, data-driven way to estimate beta. Rather than relying on fixed models or assumptions, this approach allows for sequential testing and adaptation of models over time. The goal is to identify the most suitable combination of model type and parameters (such as lookback windows or return frequency) for estimating beta at each point in time.

A typical process involves:

- Defining candidate models and cross-validation rules.

- Estimating betas on rolling samples of return data.

- Adjusting signals and position returns based on those betas.

This adaptive learning approach mirrors live trading conditions, where strategy decisions must be based only on past and current data.

Applying Beta Learning to EM Currency Strategies

A practical use case involves emerging market (EM) foreign exchange forwards. By building a strategy around real FX carry—a measure of the return adjusted for inflation expectations—traders can form positions across multiple EM currencies.

Yet many of these currencies are sensitive to global capital flows and financial shocks. Beta learning helps isolate the strategy’s intent (exploiting carry) from its inadvertent exposure to global trends. This is achieved by adjusting each currency’s carry and return based on its estimated beta relative to a global market risk basket.

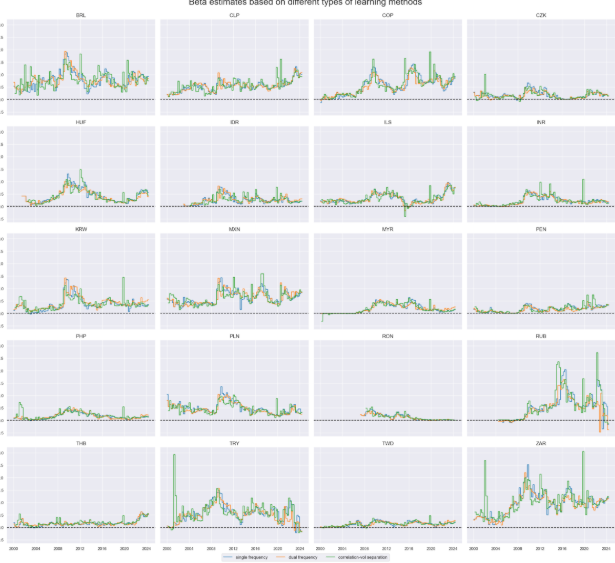

Exploring Different Learning Models

Three main beta learning frameworks were applied:

- Single-Frequency Regression: Uses either daily or weekly return data to estimate beta via linear or quantile regression. Longer lookbacks were typically favored for stability.

- Dual-Frequency Combination: Averages results from both daily and weekly regressions to benefit from their complementary strengths—frequency vs. time-zone alignment.

- Separate Volatility and Correlation Estimation: Decomposes beta into correlation and volatility ratio components, allowing independent estimation. This reflects the belief that volatility is more dynamic, while correlation is structural.

Despite differences, all models produced comparable long-term beta trends, although the single-frequency approach was more prone to short-term fluctuations.

Results: Hedged vs. Unhedged Performance

Implementing beta-adjusted hedging had a significant impact. Average correlation between EM FX returns and global market benchmarks dropped from 40% to 15%. More importantly, the hedged strategies consistently outperformed in risk-adjusted metrics like Sharpe and Sortino ratios.

While the unhedged strategy displayed strong directional bias and limited predictive power for negative returns, hedged strategies achieved more balanced and accurate forecasting. Moreover, hedged portfolios exhibited reduced seasonality and minimal correlation with global benchmarks, indicating better diversification.

Key Takeaways

- Macro beta estimation is critical in distinguishing true alpha from systemic market exposure.

- Statistical learning frameworks offer flexible, adaptive beta estimation.

- Hedging based on learned betas significantly improves the robustness and risk-adjusted performance of macro strategies.

- No single beta learning method dominates—a range of reasonable approaches yield similar benefits.

Ultimately, integrating beta learning into macro trading frameworks empowers investors to build strategies that are both more precise and more resilient to broader economic noise.